An interview about the recent surge in silver and gold, framed as a breakdown in fiat credibility rather than a breakdown in precious metals. The guest argues debt, war spending, money printing, and state-level legalization of transactional gold/silver all support a much higher long-run price for gold and silver.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

This is an interviewer-hosted conversation on Wall Street Bullion with Jason Cins, identified as the CEO of Glint. The discussion centers on the recent run-up, pullback, and renewed strength in silver and gold. The guest argues that the market is reacting to a broader macro stress environment: war-related spending, sovereign reserve sales, debt accumulation, and the likelihood of further money printing. He repeatedly frames gold as a resilience and purchasing-power asset, not just a trade. In his view, recent softness in gold is not a failure of the safe-haven function; rather, governments and institutions are using gold as a reserve they can sell in difficult times. He cites Poland, Turkey, and Russia as examples of entities selling gold for defense, currency support, or fiscal strain. He also argues that higher U.S. …

Near term, the setup is tactically bullish for gold and silver if war, deficits, or money-printer fears stay in focus. The main risk is that the move stalls again if the macro headlines cool or if the recent rally is already crowded.

Over the next few months, the base case is for precious metals to stay supported as sovereign funding needs, refinancing pressure, and inflation anxiety persist. Confirmation would come from ongoing debt expansion and renewed flows into hard assets; the view weakens if confidence in policy stabilization returns.

The long-run thesis is a slow shift from fiat confidence toward a regime where gold is treated more like monetary ballast and less like a speculative asset. If that regime shift continues, the dollar becomes less purely stable and precious metals gain structural relevance.

Gold is behaving properly as a rainy-day asset during wartime and fiscal stress.

He argues gold is being sold by governments because they are using rainy-day reserves to fund defense and stabilize currencies.

Gold has not lost its safe-haven status; the recent move reflects institutions using reserves in a crisis.

He explicitly rejects the idea that gold is failing as a hedge and says it is doing what it should do.

U.S. debt growth and refinancing needs make further money printing likely over the coming years.

He points to the jump in federal debt, large maturities, deficits, and shorter-dated borrowing as signs of structural funding stress.

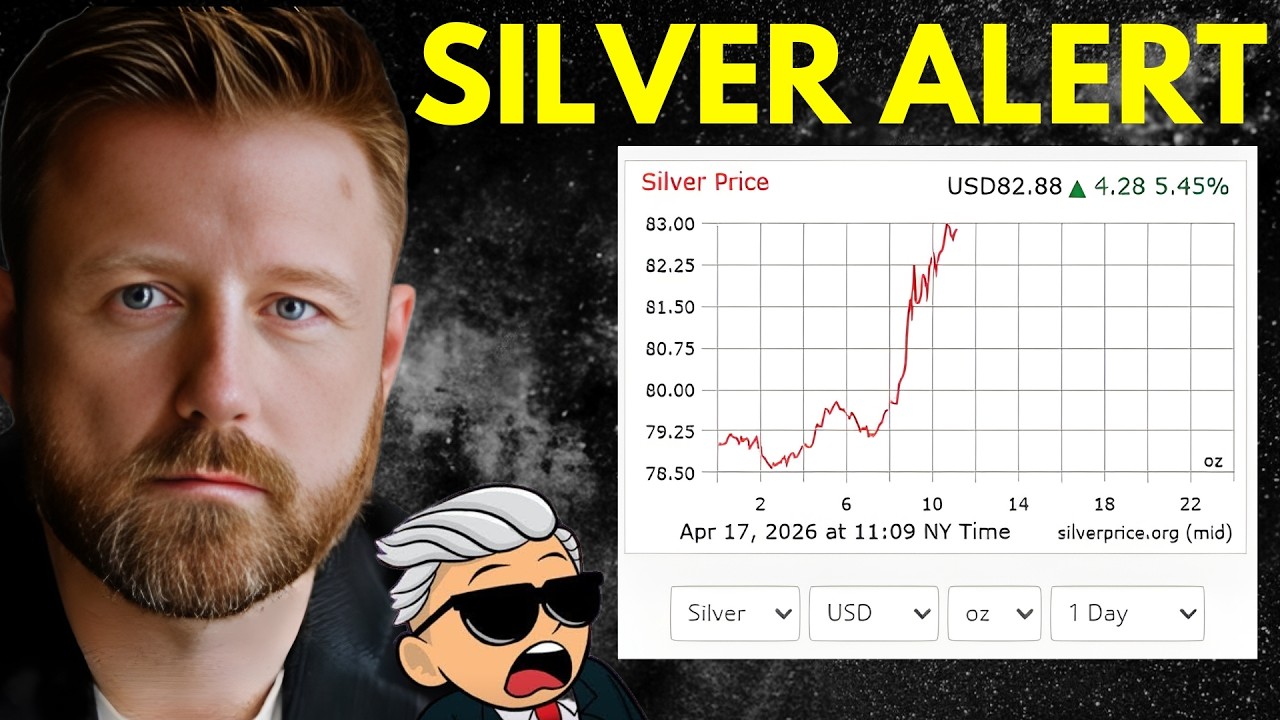

Where are we at for silver and gold right now?

Jason says the recent move should be understood through macro stress, not just price action, and that gold is behaving like a rainy-day asset being used by governments under pressure.

Do you see a point where gold is going to hit that $10,000 mark?

He says gold can reach much higher levels if money printing continues and the value of dollars and pounds keeps falling, but he does not give a precise timing model beyond debt and deficit dynamics.

Do you think America will end up back on a gold standard?

He thinks the current administration is backing stablecoins to buy time, and that state-level gold/silver legal tender laws show a slow-motion shift away from pure dollar dominance, though he stops short of predicting an official gold standard.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.