The video argues that the U.S. yield curve’s recent steepening is a historically ominous recession signal, but says the usual sequence has not fully played out yet because jobless claims and corporate profits remain strong. The speaker’s base view is that the economy may still avoid recession in the near term and that stocks can keep grinding higher, especially if profits stay elevated and unemployment stays low.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

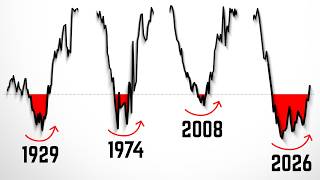

The core thesis is that the yield curve has steepened in a way that has historically preceded recessions, but the speaker thinks this time may be different because the labor market and corporate profit backdrop are still unusually strong. They frame the current setup as a “very scary signal” without turning it into a full bearish call, arguing instead that investors should understand what the indicator is saying and position more intelligently rather than “sell all your stocks and start hoarding cash.” The speaker leans heavily on historical precedent. They say the yield curve has steepened by two full percentage points after an inversion and cite prior episodes including the early 1980s, the 2020 pandemic recession, the 2007 financial crisis, the 2001 dot-com bust, the 1990 Gulf War recession, and even the Great Depression. …

Tactically, the near-term setup is still constructive unless claims or profits roll over; the main immediate risk is a renewed inflation pulse that pushes the Fed back toward tighter policy. The video’s own read is that the market can keep trending higher for now, but the next few months are the key test.

Over the next several weeks to months, the base case is continued expansion if labor data stays benign and earnings remain firm, with growth potentially improving as the lagged effects of easier credit filter through. That view weakens quickly if unemployment, claims, or profits begin to deteriorate.

Structurally, the speaker is arguing for a regime where the yield curve still matters, but only as part of a broader credit-plus-labor framework rather than a standalone crash trigger. If this cycle avoids recession, it would support the idea that macro timing signals can be delayed by unusually strong corporate balance sheets and labor resilience.

Every single time the yield curve has steepened like it is today, it was either during or right before a recession began.

The speaker lists historical instances (2020, 2007, 2001, 1990, 1929) where yield curve steepening preceded or coincided with recession.

Corporate profits remaining at record highs despite yield curve inversion means businesses have no pressure to cut costs and lay workers off, so economic growth could hold up in the 3-month danger window.

The speaker argues that the usual recession mechanism (falling profits → layoffs) is absent because profits are at all-time highs, so the yield curve signal may not materialize into recession this time.

In the vast majority of past instances where the yield curve steepened, a recession typically began within 12 months of the yield curve crossing back above the zero threshold.

The speaker observes historical patterns and then notes that the current crossing happened in June 2025 (12 months ago) but a recession has not occurred yet, creating uncertainty.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.