Lynette Zang argues that gold and silver’s recent moves are being driven more by speculative paper contracts than by physical demand, and she sees the larger setup as a breakdown in fiat confidence and a transition toward a supply-and-demand pricing regime for precious metals.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

The conversation centers on Lynette Zang’s view that the recent volatility in gold and silver is not mainly about the underlying physical metals, but about paper/spot contracts becoming overheated and then correcting back toward the 200-day moving average. She says the physical market is the true safe-haven market, while spot contracts have become a speculative trade, and she repeatedly distinguishes paper pricing from physical demand. Zang frames central banks as accumulating physical gold for balance-sheet safety and freedom from counterparty risk, while ordinary investors should treat physical possession as the point of ownership. The host asks about Russia, Turkey, COMEX inventories, China’s physical buying, and what could happen if delivery fails. …

Tactically, the setup is for continued volatility in gold and silver paper prices with downside risk as overheated moves normalize, but any delivery stress or premium spike could flip the tape fast. For traders, the key near-term watch is physical scarcity versus spot weakness, not just chart momentum.

Over the next few months, the base case in her framework is that physical demand gradually asserts itself over paper pricing as confidence and liquidity become more fragile. The setup improves if premiums widen, delivery stress persists, or policy response turns more accommodative; it weakens if the paper market keeps absorbing stress cleanly.

Structurally, she is calling the end of the fiat-confidence regime and the reassertion of hard assets as reserve anchors. In that world, physical gold remains the long-duration wealth-preservation asset, while silver carries added barter and scarcity optionality.

The recent move in gold and silver was driven mainly by spot/paper contracts rather than the physical market.

Lynette says the confusion comes from treating spot contracts as the metal itself and argues the move became a speculation trade.

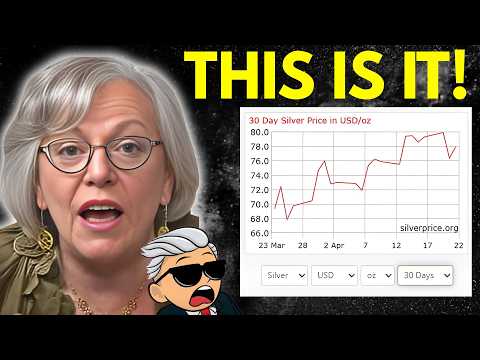

Silver and gold had become stretched above their 200-day moving averages, which suggests a speculative excess and helps explain the correction.

She uses the 200-day moving average as a benchmark and says silver was far above it, making a reversion likely.

Central banks prefer physical gold because it carries no counterparty risk and protects freedom.

She says central banks hold physical metal rather than contracts for safety and sovereignty reasons.

What are your thoughts right now on silver and gold given conflicting views about why they have or have not moved during global conflict?

Lynette says the discussion should focus on spot contracts versus physical metal. She argues that the move was speculative, stretched above the 200-day moving average, and that physical gold is the real flight-to-safety asset held by central banks.

Why are countries like Russia and Turkey selling so much gold?

She says it is tied to war, sanctions, and the need to protect purchasing power and savings. Gold is described as emergency savings if access to the banking system is disrupted.

What happens if COMEX cannot deliver on its gold or silver contracts?

She says the system may first be papered over with fiat settlement or a premium payment, but if delivery cannot be met, a force majeure or similar event could reveal the true price of gold and silver and cause a spike.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.