Peter Schiff argues that the April jobs report and broader economic narrative are misleading, with weak labor quality hidden by survey quirks, falling full-time employment, and political incentives to overstate strength. He then pivots to markets, saying stocks are priced for a perfect end to the war and an AI boom that is already overhyped, while remaining bullish on gold, silver, copper, and miners.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

Schiff opens by saying he had planned a regular Friday market wrap and will focus on jobs, war, and markets, with gold and silver included. His central argument on labor is that the April jobs report was presented as a beat, but the headline number is weak in context and, more importantly, unreliable. He says the establishment survey showed +115,000 jobs, but the household survey showed -226,000 jobs, and he prefers the household survey because it better matches reality. He emphasizes that labor force participation fell to 61.8%, the unemployment rate is artificially low because people leaving the labor force are no longer counted as unemployed, and average hourly earnings are rising slower than prices, so real wages are falling. …

Near term, the actionable risk is that stocks are leaning too hard on war-optimism and AI enthusiasm while the jobs narrative looks softer under the hood. If oil fails to collapse or the peace story stalls, the current equity bid could unwind quickly.

Over the next few months, the more likely path in Schiff’s framework is a weaker labor-market narrative, continued skepticism around AI-driven capex returns, and pressure on equities if yields rise and the war premium persists. Confirmation would come from further labor revisions, weaker full-time employment, and less impressive AI monetization.

Structurally, this is a regime where real technology coexists with inflated financial claims: AI can be transformative while the linked stocks and infrastructure spend still disappoint. Schiff’s broader long-term thesis is that hard assets outperform as official data, policy credibility, and valuation discipline deteriorate.

The April jobs report was a weak number despite beating expectations, and the headline beat is being oversold as proof of economic strength.

He argues 115,000 jobs is not a strong figure and that the market/media are framing it as stronger than it is.

The labor market is weaker than the establishment survey suggests because the household survey showed a 226,000 decline in employment and full-time jobs fell sharply while part-time jobs rose.

He uses the household survey, full-time/part-time split, and participation data to argue the underlying labor market is deteriorating.

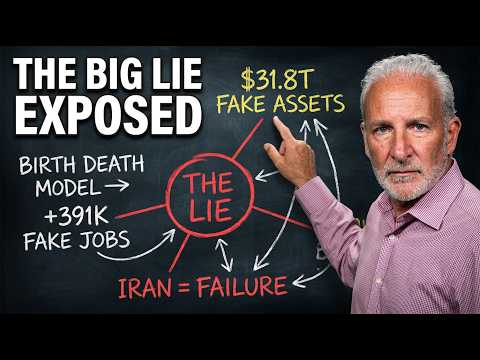

The birth-death model is overstating job creation and may mean the reported gains are largely fictional.

He says 391,000 jobs came from the birth-death model, which he views as guesswork biased too high.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.