Peter Bookvar argues the recent pullback in gold and silver is likely closer to ending than beginning. He says the selloff was driven less by a broken precious-metals thesis and more by liquidity, higher real rates, a stronger dollar, and forced selling from countries under energy stress, while the long-term bull case remains intact via central-bank diversification and silver’s industrial demand.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

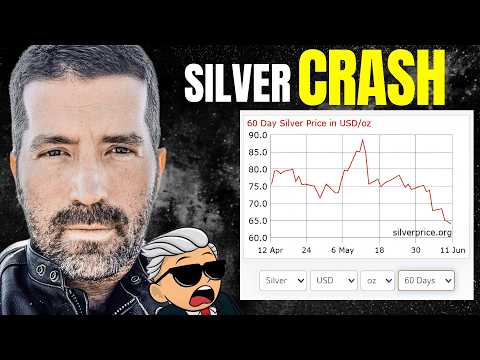

This interview centers on whether the sharp correction in gold and silver is a buying opportunity or the start of a bigger trend change. Peter Bookvar’s core view is constructive: he thinks the market is probably closer to the end of the pullback than the beginning, and that current levels are reasonable for “nibbling” back into precious metals for investors who missed the rally or want to re-enter. He explicitly notes that silver is still down nearly 50% from its highs, so the move has already been severe, even if further chop remains possible. His explanation for the selloff is mostly technical and flow-driven rather than a collapse in the underlying thesis. He says gold was “being liquidated for liquidity purposes,” effectively trading with equities, and points to the 14-day RSI reaching its lowest level since 2024 and a gold-miner technical index falling to zero. …

Tactically, the metals look like they may be finishing a corrective flush rather than starting a new leg down, so small-scale re-entry looks favored over chasing strength. The main near-term risk is that real yields or the dollar keep rising and extend the chop.

Over the next few weeks to months, the more likely path is consolidation and rebuilding rather than a straight rally or a deeper breakdown. That view holds unless higher rates, renewed dollar strength, or persistent forced selling reassert pressure on the metals.

Structurally, the speaker is still bullish on precious metals because central-bank diversification and hard-asset demand appear durable. He also sees a wider regime in which non-dollar exposure and real assets matter more as sovereign-bond skepticism grows.

The pullback in gold and silver is probably near its end, and current prices are reasonable for nibbling back in.

He directly says they are closer to the end of the pullback and that current levels are good to start nibbling again.

The recent gold selloff was largely a liquidity-driven liquidation rather than a fundamental breakdown.

He says gold was being liquidated for liquidity purposes and followed the S&P lower.

Rising real rates and a stronger dollar were headwinds for gold over the last couple of months.

He explicitly names real rates and the dollar as fundamental headwinds.

What's happening right now with precious metals — why did silver and gold drop so much and are they starting to recover?

Peter explains that gold was being liquidated for liquidity purposes, following the S&P, with the 14-day RSI reaching the lowest level since 2024 and gold miner technicals hitting zero. He notes they sold most of their silver in late December anticipating consolidation after parabolic moves. He points to fundamental headwinds like rising real rates and a strong dollar, plus gold being sold by countries that own gold and also import energy. He believes the worst of the declines may be over and silver is down nearly 50% from highs.

Why isn't gold reacting the same way as before during times of war and financial uncertainty — is this just a liquidity crunch or people flooding to the dollar?

Peter says the algos focus on where real rates are going and where the dollar is. The rise in interest rates has been on the real rate side, not inflation break-evens, creating a headwind. Gold has also been a source of funds for liquidity. He notes gold had an extraordinary move higher and from a chart perspective you don't want to see something go vertical — and looking back, that was the end of this move. He believes the mega trend of central banks diversifying is still intact for the long term, but short-term other factors are at play.

Are there any warning signs flashing right now that concern you — whether in bonds, interest rates, debt levels, or debt servicing?

Peter points to US, UK, French, German, and Japanese long-end interest rates rising in concert, which he sees as investors pushing back on owning long-duration sovereign bonds — potentially due to worries about debts and deficits and central banks having negative or barely positive real rates. He notes the US 10-year at 4.5% has been an important level, and the equity market is more comfortable with yields below that threshold.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.