The guest argues that precious metals have already entered a major unwind and that the more sensible place for capital is in productive businesses with earnings, dividends, and buybacks. He says gold and silver were overhyped, have already fallen sharply, and are not safe havens in the way promoters claim.

Watch on YouTube ›Get the market thesis, key claims, assets, contradictions, and follow-up questions from any financial video — then unlock a version personalized to your portfolio, watchlist, and favorite speakers.

The core thesis is blunt: silver and gold are not reliable stores of value, are not “productive,” and should not be treated like serious long-term investments when compared with cash-flowing companies. Father Emanuel Lemelson says he warned earlier in the year that precious metals were in a bubble-like setup and now points to the declines in gold and silver as validation, arguing that the metal trade has already started to collapse rather than resume a durable bull leg. He frames the current market as an overextended, manipulated “open casino” where many participants—especially younger investors—are treating markets like a prediction game rather than a discipline of capital allocation. He links this to broader social malaise: people facing housing costs, student debt, and weak job prospects may feel forced into speculation. …

Tactically, the setup is bearish for silver and gold: the speaker thinks the recent drawdown is the beginning of a deeper unwind and does not want viewers chasing the metals dip. Near-term risk is continued de-rating if the market keeps ignoring the war/debt narrative.

Over the next few months, he expects productive, shareholder-friendly equities to outperform inert stores of value unless precious metals regain momentum despite the current macro noise. The key test is whether metals can reverse the slide and reclaim the safe-haven bid he says is missing.

Structurally, the speaker is arguing for a regime where capital should favor operating businesses over non-productive assets. His longer-term view is that durable wealth comes from earnings, dividends, and buybacks, while metals remain vulnerable to valuation skepticism and speculative cycles.

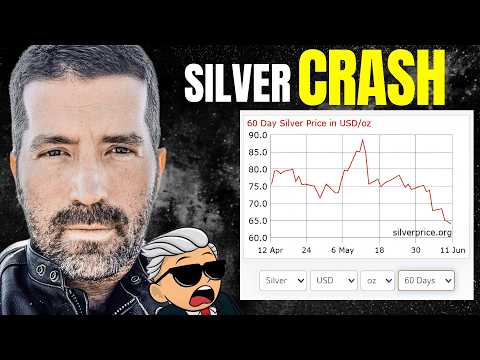

Precious metals are not a safe haven because gold is down 25% and silver down 50% in a few months, proving they are not a stable store of currency.

The speaker argues that extreme volatility in precious metals contradicts the 'safe haven' narrative.

Gold and silver were essentially akin to a bubble and set to collapse as of late January 2025.

The speaker notes that since his January 29th warning, gold is down 25% and silver down 50%, which he presents as confirmation.

Harley-Davidson has a shareholder yield of about 16% between buybacks and dividends, making it a profoundly misunderstood productive asset trading at a fraction of its worth.

The speaker cites the high shareholder yield and long history of profitability, suggesting the market misprices the company.

Is there anything in the markets right now that's concerning you?

The guest says the market has been concerning him for a long time, reaching historic highs in how expensive it became. He describes it as an 'open casino' — a manipulated market where the political system openly manipulates it, and a generation of young people has come to see capital allocation as akin to a prediction market, wanting to 'roll the dice' to get rich quick.

Where should we be putting our money right now to see good returns or help our portfolio?

The guest argues for productive assets that pay dividends and return capital to shareholders, citing the 4.5% risk-free rate on 10-year Treasuries. He recommends General Mills (stable dividend, long track record), Adobe (generation opportunity in SaaS), and Harley-Davidson (~16% shareholder yield from buybacks and dividends). He contrasts these with precious metals, which he calls 'sterile assets' requiring storage and insurance costs that have seen gold down 25% and silver down 50% since January.

How does the war with Iran and Israel and the US affect the markets long term?

The guest calls it a horrible failure of humanity, says Americans should feel ashamed at our role in the death of innocents, and finds it hard to speak in purely economic terms because you can't put a price on one innocent life. However, he acknowledges that historically war is stimulative and that's what economists will say.

Unlock the full claims, asset map, scores, related transcripts, follow-up questions, and AI chat — shaped around your portfolio, watchlist, favorite speakers, and risks.